Last month, I had the opportunity to attend Connected Germany in Munich, a key event for anyone involved in the nation’s telecommunications landscape. The atmosphere was buzzing with conversations about the future of digital infrastructure. But what’s really changed in Germany’s journey towards comprehensive connectivity?

The first day was heavily focused on the fibre broadband business, though the initial keynote, delivered by Andreas Walter and Peter Winzer from Dialogue Consult GmbH, provided a comprehensive overview of both the fixed and mobile network landscapes. Their presentations set the stage for a day of deep discussion, revealing a complex picture of progress, historical challenges, and a cautiously optimistic path forward.

This post will unpack the key takeaways from the conference, exploring the unique context of Germany’s digital evolution and what it means for the future of its fixed-line and mobile networks.

Germany’s Lingering Allegiance to Copper

To understand the current state of Germany’s fibre network, one must look at its history. Unlike many of its European neighbours who pivoted to fibre earlier, Germany fully committed to copper DSL technology. Deutsche Telekom rolled out an extensive VDSL (Very-high-bit-rate Digital Subscriber Line) network, upgrading the existing copper lines to deliver download speeds of up to 200 Mbps to most households.

This strategic decision has had two major consequences that continue to shape the market today.

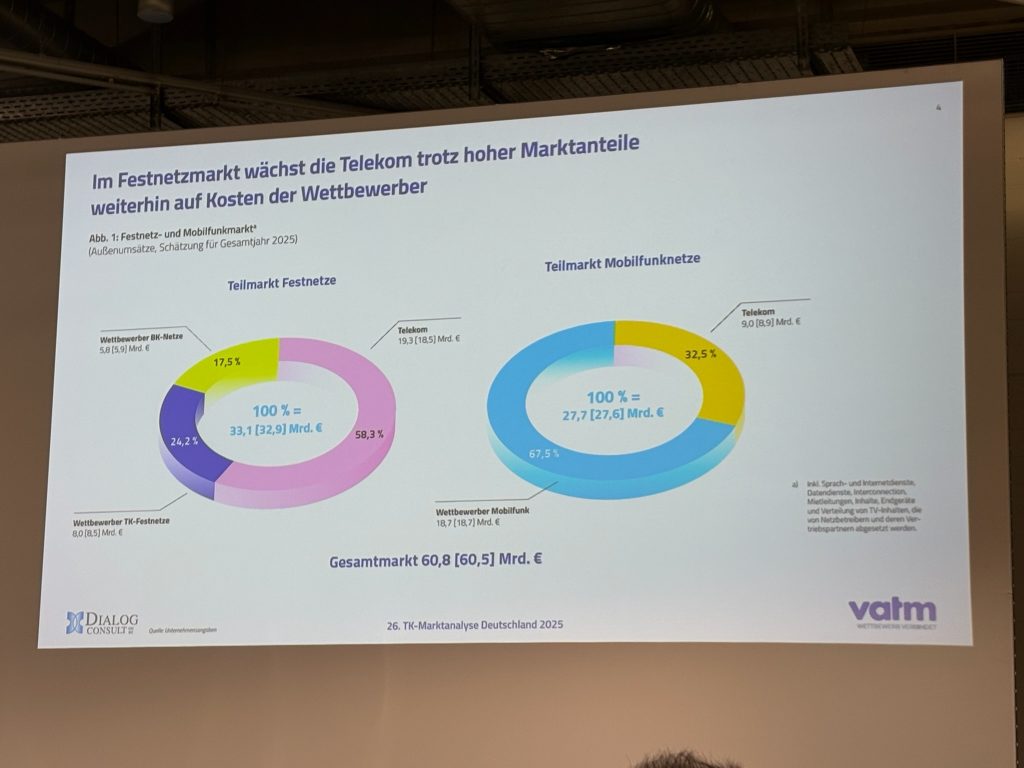

First, Deutsche Telekom made a significant upfront investment in its VDSL network. Now, the company can simply “sweat the asset,” continuing to generate revenue from a technology that has already been paid for. In fact, based on figures shared at the conference, Deutsche Telekom still earns more from providing connectivity over its copper network than it does from switching customers to fibre. This financial reality reduces the incentive for the incumbent to aggressively push for a nationwide fibre-to-the-home (FTTH) rollout.

Second, with download speeds of 200 Mbps, the connectivity needs of most German households are already met. For the average user, there isn’t a compelling, experience-driven reason to upgrade to fibre. This creates a significant challenge for alternative network providers (altnets) trying to build a business case for their fibre investments.

The Challenge of Customer Inertia and Open Access

A fascinating insight came from an analyst who presented market research, reportedly sponsored by VATM (the German Association of Telecommunications and Value-Added Services). The study highlighted a strong reluctance among German consumers to switch providers. While they might be interested in the superior technology of fibre, the idea of moving away from a familiar company is often a step too far.

However, these same consumers would consider upgrading to fibre if it were offered by their current provider. This finding strongly supports the idea that open access is the most viable path forward for fibre providers. Instead of competing at a crowded retail level, fibre builders can focus on filling their networks by wholesaling access to other service providers, including the dominant players. This model allows consumers to get the best technology without the perceived hassle of changing their service provider.

Despite the rise of altnets, Deutsche Telekom remains the dominant force in the fixed broadband market, holding nearly 60% of the market share. The investor mood has palpably shifted, moving away from a singular focus on “homes passed” (the number of homes a network reaches) to “homes connected” (the number of paying customers). This change puts immense pressure on operators to monetise their infrastructure. In this context, much of the conference’s focus was on standardising networks to facilitate wholesale purchasing and interconnection, making open access a practical reality.

The Mobile Market: A More Level Playing Field

In contrast to the fixed broadband market, Germany’s mobile landscape is more evenly distributed among operators. This is also rooted in history, as Germany has had service providers akin to Mobile Virtual Network Operators (MVNOs) from the very beginning, fostering a more competitive environment.

However, the mobile sector faces its own challenges. A significant geopolitical shift is underway, with growing questions about the use of Chinese vendors in German networks. This could trigger a massive network swap-out, with a deadline for completion set for 2029.

Furthermore, 1&1 has now finalised its migration off the Telefónica O2 network and is focused on establishing itself as the country’s fourth major mobile operator. Its primary challenge will be to build out its own network coverage to compete effectively with the established incumbents.

Bavaria’s Bid to Become a Digital Hub

Despite these developments, international reports consistently place Germany in the lower ranks for digital adoption. Shockingly, some outdated practices persist; for instance, certain official communications between operators are only considered valid if sent by fax.

Against this backdrop, the speech by Dr. Hans Michael Strepp, Bavaria’s Minister for Digital Affairs, was particularly inspiring. He affirmed Bavaria’s commitment to digital transformation through its ambitious Hightech Agenda Bavaria. The state is actively reviewing its administrative processes to simplify or eliminate steps that hinder digitisation.

Dr. Strepp announced that Bavaria is investing €5 billion in this agenda—more than all other German states combined. The goal is to position Bavaria as a digital powerhouse. This ambition was recently bolstered by the announcement that the region will become a Digital Innovation Hub (DInA), signalling a clear intent to lead Germany’s digital future.

A Street-by-Street Battle for a Digital Germany

The overall atmosphere at Connected Germany was one of determined optimism. There was a strong focus on collaboration and a “can-do” attitude to overcoming the nation’s digital hurdles.

However, the dream of rapidly delivering scalable, nationwide fibre broadband remains distant. The process is less of a revolution and more of a “street-by-street battle.” While the ambition is there and significant investments are being made, historical infrastructure decisions and consumer behaviour present formidable obstacles. The journey to a fully digitised Germany will be a marathon, not a sprint, requiring sustained collaboration between operators, investors, and policymakers.